The concept of revised returns is not provided in the GST return rules and accordingly, the businesses would have to avail and re-avail, the mismatched credit by way of credit notes, debit notes, and supplementary invoices. The return rules have prescribed different forms to be filled by a registered person. The persons registered under the existing state VAT Acts would be familiar with the concept of ‘matching principle of ITC’. In this the ITC claimed by the recipient of taxable goods and/or services is matched with the outward supply of taxable goods and/or services as claimed by the supplier. This matching, reversal and reclaim of ITC amount is made available through the following steps:

Details are obtained through valid returns filed by both supplier and recipientMatching and finding discrepancyCommunication of discrepancy to both supplier and recipientRectification of discrepancyReclaim where discrepancy is rectified within the given timeframe

Matching of input tax credit:

Section 42(1) of the CGST Act, 2017 the details of every inward supply furnished by a registered person (hereafter in this section referred to as the “recipient”) for a tax period shall, in such manner and within such time as may be prescribed, be matched–

(a) with the corresponding details of outward supply furnished by the corresponding registered person (hereafter in this section referred to as the “supplier”) in his valid return for the same tax period or any preceding tax period;(b) with the integrated goods and services tax paid under section 3 of the Customs Tariff Act, 1975 in respect of goods imported by him; and(c) for duplication of claims of input tax credit.

As per Rule 69 of the CGST Rules, 2017 the following details relating to the claim of input tax credit on inward supplies including imports, provisionally allowed under section 41, shall be matched under section 42 after the due date for furnishing the return in FORM GSTR 3

(a) GSTIN of the supplier;(b) GSTIN of the recipient;(c) invoice or debit note number;(d) invoice or debit note date; and(e) tax amount:

Details are obtained through valid returns filed by both supplier and recipient

FORM GSTR-1 and FORM GSTR-2A Details of outward supply of goods and/or services are filed by supplier in FORM GSTR-1, which would be available to recipient in FORM GSTR-2A FORM GSTR-2 AND FORM GSTR-1A Details of inward recipient of goods and/or services are filed by recipient in FORM GSTR-2, which would be available to supplier in FORM GSTR-1A for him to accept or modify the changes. FORM GSTR-3 Monthly return to be filed by a registered person mentioning details of inward and outward supply of goods and/or services, ITC claimed along with taxes payable and paid thereof.

2. Matching and finding discrepancy

When FORM GSTR-3 is submitted by both the supplier and recipient, the following details are matched:

3. Communication of discrepancy to both supplier and recipient

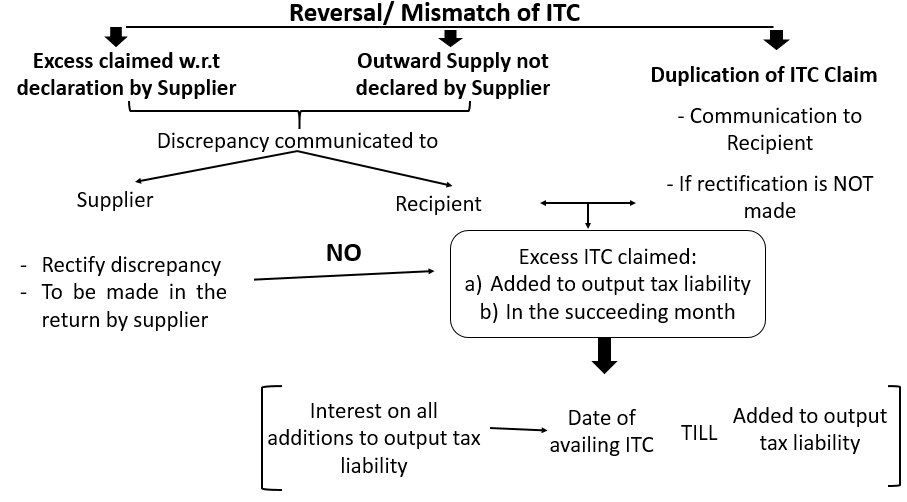

In case the details furnished by both do not match, such discrepancies will be communicated to both the supplier and recipient, or just the recipient depending on the nature of discrepancy, after filing of FORM GSTR-3. Discrepancy of ITC arises in the following situations:

ITC claimed by recipient is in excess of the tax declared by the supplier, orthe outward supply is not declared by the supplier, orthere is a duplication of claim of ITC by the recipient

4. Rectification of discrepancies

If a discrepancy arises, it can be rectified in the following ways: As per Rule 71(2) of the CGST Rules, 2017 a supplier to whom any discrepancy is made available under sub-rule (1) of rule 71 may make suitable rectifications in the statement of outward supplies to be furnished for the month in which the discrepancy is made available. As per Rule 71(3) of the CGST Rules, 2017 a recipient to whom any discrepancy is made available under sub-rule (1) of rule 71 may make suitable rectifications in the statement of inward supplies to be furnished for the month in which the discrepancy is made available. If the recipient or the supplier has rectified the error, the inward supply and outward supply will match and credit will be finally accepted. In case of discrepancy of claim w.r.t. declaration by supplier in his valid return, such discrepancy shall be communicated to supplier and recipient. On receipt of such a communication, the supplier shall be asked to rectify the discrepancy in his valid return for the month in which discrepancy is communicated. If the supplier does not rectify the discrepancy, the excess ITC claimed earlier shall be added to the output tax liability of the recipient in the next month For example: If the discrepancy is communicated in the month of July and not rectified by supplier, then the ITC claimed earlier shall be added to the output tax liability of the recipient for the following month of August. 2. Duplication of claim of ITC by recipient In case of a duplication of claim, the recipient will be intimated about the duplication of claim. If a rectification is not made, then the ITC claimed earlier shall be added to the output tax liability of the recipient for the month in which duplication communicated For example: Assuming that the intimation about the duplicate claim was sent in the month of July, the ITC claimed earlier shall be added to the output tax liability of the recipient in the month of July itself if the rectification is not made in time. In case of additions, the recipient shall be required to pay an interest not exceeding 18% on the amount added to the output tax liability from the date of availing the ITC till the additions are made in returns.

5. Re-Claim of ITC

It means that the recipient has claimed credit second time. As per Rule 72 of the CGST Rules, 2017 duplication of claims of input tax credit in the details of inward supplies shall be communicated to the registered person in FORM GST MIS-1 electronically through the common portal. Any interest paid earlier on excess claim of ITC will be refunded by crediting the amount to the recipient’s Electronic Cash Ledger. In case of duplication of ITC claim, no refund will be allowed as it is a contravention of the GST provisions. For example: Mr. Anand, the recipient, files his FORM GSTR-3 on 18th September 2017, for the tax period of August 2017. On matching, a discrepancy is found in the inward supply furnished by him in FORM GSTR-2 for Rs 10,000. The ITC claimed on this is Rs. 1,200. Now, this discrepancy is communicated to Mr. Anand and his supplier. The supplier refuses to make the rectification in his valid return. So, the availed ITC of Rs. 1,200 will be added to Mr. Anand’s output tax liability for the tax period of September 2017 and interest will be payable on this. Now, if the supplier rectifies the discrepancy through debit note or invoice within the specified time frame, Rs. 1200 will again be allowed as ITC and the amount paid as interest will be refunded.