Latest Amendment by Budget 2017

It is proposed to insert a new section 92CE in the Income Tax Act to provide that a taxpayer would be required to carry out a secondary adjustment where a primary adjustment to transfer price has been made in certain stipulated circumstances.The second adjustment would be made only if the following conditions are satisfied:the primary adjustment is INR 10 million (USD 148,372[1]) or more, andthe excess amount attributable to the adjustment is not repatriated to India within the prescribed time.Secondary adjustment can be made in following cases wherethe primary adjustment to transfer price has been made suo-motu by the assessee in his return of income; orthe primary adjustment to transfer price made by the Assessing Officer has been accepted by the assessee; orthe primary adjustment to transfer price is determined by an advance pricing agreement entered into by the assessee under section 92CC; orthe primary adjustment to transfer price is made as per the safe harbour rules framed under section 92CB; orthe primary adjustment is arising as a result of the mutual agreement procedure under section 90 or 90A.

ANALYSIS WITH PRACTICAL ILLUSTRATION

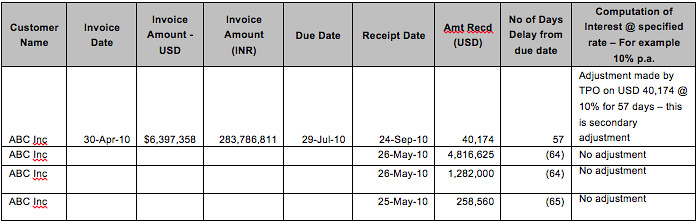

Refer ANNEXURE A

Key Analysis

“Secondary adjustment” means an adjustment in the books of accounts of the assessee and its associated enterpriseto reflect that the actual allocation of profits between the assessee and its associated enterprise.The actual allocation need to be consistent with the transfer price determined as a result of primary adjustment,thereby removing the imbalance between cash account and actual profit of the assessee.As per the OECD’s Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations (OECD transfer pricing guidelines), secondary adjustment may take the form of constructive dividends, constructive equity contributions, or constructive loans.A number of leading economies in the world use this rule as a method to align the economic benefit of the transaction with the arm’s length position.Pursuant to this adjustment, the excess amount which is available to the related party as a result of the adjustment but is not repatriated to India within the prescribed timeline, shall be deemed to be an advance made by the taxpayer to the related party and the interest on the advance shall be considered income of the taxpayer.The prescribed time is not defined as of now. Few of the options possible for prescribed timeline are: «the below options are illustrative only for understanding – the government may provide any timeline»Time provided under Foreign Exchange Management Act, 1999Time allowed in agreement entered between related partiesTime allowed in transaction between taxpayer and independent third party,Any other standard tine, etc.The secondary adjustment is already made by the Income tax Authorities. As of now, the adjustment is made in the following cases:Outstanding receivables;Valuation of shares, etc.

[author title=”About Author” image=”https://caknowledge.com/wp-content/uploads/2017/02/CA-Anuraag-Singhaal-Author-at-CAknowledge.in_.jpg”]

Anuraag Singhaal CA (2005) & CPA (USA)(2008) 11 Years of Work Experience with PwC (Big 4), Deloitte (Big 4), Reliance Industries Group Best-in-class Faculty for Direct Taxes (DT) CA Final For Batches & Sessions, contact at 9582039221 [/author] Practical Discussion On Secondary Adjustment On Outstanding Receivables In my practical experience, I had seen this secondary adjustment for first time TP in assessment of AY 2009-10.Now, let us consider an example. The debtors outstanding in the balance sheet of the taxpayer. For example if the assessment is made for AY 2011-12, the Transfer Pricing Officer (TPO) would call for information of debtors outstanding as on March 31, 2011. The details are generally called in the following format:Refer ANNEXURE AThe adjustment is used to be made for the time since the invoicing is done till collection is made excluding the grace period allowed under the agreement or allowed by TPO.There are various case laws where it has been held that secondary adjustment on account of interest for delayed collection of receipts cannot be made because from a business point of view, the interest is also factored/ subsumed in the sales price. Case LawRelevant GistMicro Inks Ltd. [144 ITD 610/36 taxmann.com 50 (Ahd – Trib)]This adjustment must be deleted for the short reason that it was part of the arrangement that specified credit period was allowed and thus the cost of funds blocked in the credit period was inbuilt in the sale price.Evonik Degussa India Private Limited (ITA No. 7653/MUM/2011)Moreover, the T.P. adjustment cannot be made on hypothetical and notional basis until and unless there is some material on record that there has been under charging of real income.Bharti Airtel Ltd. Vs. ACIT [ITA No. 5816/Del/2012]..But the core issue before us is whether such a deeming fiction is envisaged under the scheme of the transfer pricing legislation or on the facts of this case. We donot find so. We do not find any provision in law enabling such deeming fiction In some of the cases, the secondary adjustment has been deleted where taxpayers have proved that credit period allowed to AE debtors is less than credit period allowed to non-AE debtors. In other words, outstanding receivables from AE debtors are collected earlier as compared to the collection period of non-AE debtors. Case LawRelevant GistIndo American Jewellery Limited vs. DCIT [ITA No.5872/Mum/2009]It was held that in case no interest is charged from AEs as well as non-AEs on outstanding receivables, no addition on account of such interest can be madeLintas India Pvt. Ltd. Vs. ACIT-3(2), Mumbai [TS-713-ITAT-2010(Mum)-TP]Since assessee is not charging interest to any client on the transactions for the credit period available, in our view the facts does not require charging of interest on the credit period made available to AE. Since it is a practice of assessee not to charge interest to any client, this aspect should not be considered as an international transaction exclusively in the case of AE In some cases, it is held that adjustment for imputed interest (secondary adjustment) should be applied considering LIBOR. Case LawSiva Industries & Holdings Ltd (ITA No. 2148/Mds/2010)Four Soft Ltd. (ITA No. 1495/HYD/2010)Apollo Tyres Ltd. (I.T.A No.616/Coch/2011) Date from which amendment is applicable à e.f. 1st April, 2018 and will apply in relation to the assessment year 2018-19 and subsequent assessment years. Annexure A [1] converted at INR 67.3981 =USD 1 Recommended Articles Transfer Pricing – Meaning, Methods, Compliances, Penalties, ReportTransfer Pricing Definition & Transfer Pricing MethodsTransfer Pricing Case StudiesList of All Incomes Exempted from Income Tax, List of Exempted IncomesRestriction on set-off of loss from House property : Section 71(3A)

In some cases, it is held that adjustment for imputed interest (secondary adjustment) should be applied considering LIBOR. Since it is a practice of assessee not to charge interest to any client, this aspect should not be considered as an international transaction exclusively in the case of AE Date from which amendment is applicable à

e.f. 1st April, 2018 and will apply in relation to the assessment year 2018-19 and subsequent assessment years.

Annexure A [1] converted at INR 67.3981 =USD 1 Recommended Articles

Transfer Pricing – Meaning, Methods, Compliances, Penalties, ReportTransfer Pricing Definition & Transfer Pricing MethodsTransfer Pricing Case StudiesList of All Incomes Exempted from Income Tax, List of Exempted IncomesRestriction on set-off of loss from House property : Section 71(3A)